Insuring an EV in the US runs far higher than a comparable gas car.

Massachusetts owners pay 54% more to cover an EV than a gas model.

A few states quietly flip it, making EVs the cheaper car to insure.

The price gap between combustion cars and their electric equivalents keeps shrinking, but an EV will still hit your wallet harder than an ICE model at the dealership. The cost doesn’t stop there. Insuring one runs much steeper too, according to a new study from Insurify.

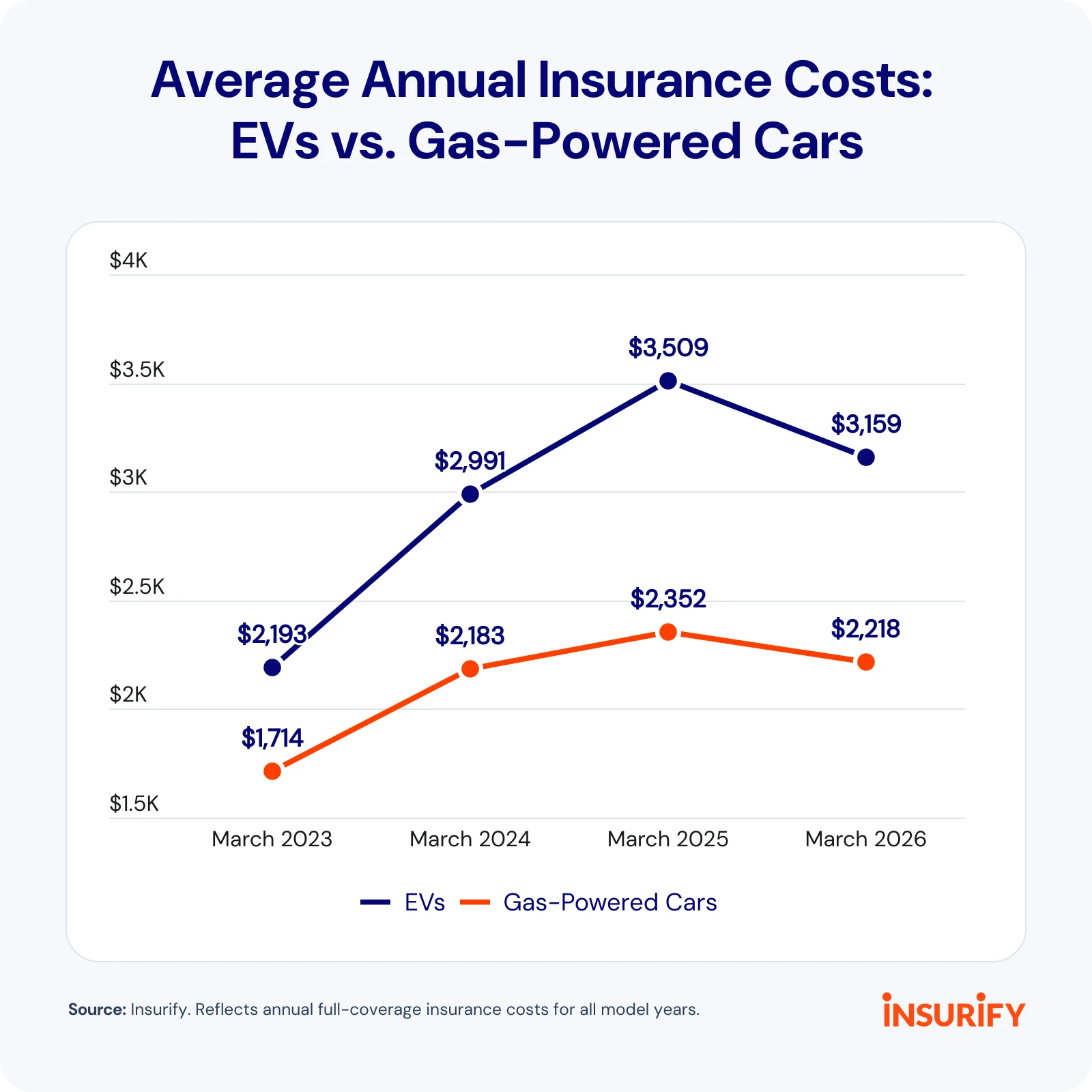

Currently, the average cost to insure an EV in the US is an eye-watering $3,159. While that’s down significantly from a peak of $3,509 in March of last year, it still far exceeds the average annual insurance cost for a gas-powered car, now $2,218, a 42 percent difference. The gap starts to close, though, when you dive a little deeper into the data.

The average EV on US roads is much newer than the average ICE vehicle, simply because electric cars haven’t been around as long. Insurify pegs the median age of vehicles in its database at 11.5 years, with older gas models dragging the overall figure down.

So it comes as no surprise that the typical EV costs more to insure than its gas counterpart. The gap narrows sharply to just 18 percent when comparing 2024 and newer vehicles across all powertrains. There, the average premium is $3,293 for an EV versus $2,792 for a gas-powered alternative.

Insurance premiums vary widely depending on where you live. Insurify’s analysis, which measures more than 235 million insurance rates across its database, shows that in some states the difference between insuring a 2024 or newer EV and a comparable ICE can run upwards of 50 percent.

Washington, D.C. is the costliest location in the data, averaging $6,102 for newer EVs and $4,821 for newer gas-powered cars.

EV owners in Massachusetts also feel the pinch. While the average annual premium for a newer EV is $3,560, it’s just $2,318 for a new ICE, making the gas car 54 percent cheaper. Insurify points to dense urban exposure, higher-value vehicles, and elevated EV repair labor costs as key factors in Massachusetts. In New York the difference is 45 percent, with EV premiums at $4,531 against $3,135 for a comparable gas model, higher than what Massachusetts drivers pay.

Premiums in Rhode Island are egregious in their own right. Annual averages for new EVs currently sit at $6,043 against $4,344 for newer ICE models, making the gas cars 39 percent cheaper to insure. The state has also seen auto insurance costs jump 41 percent since the start of 2024, according to Insurify.

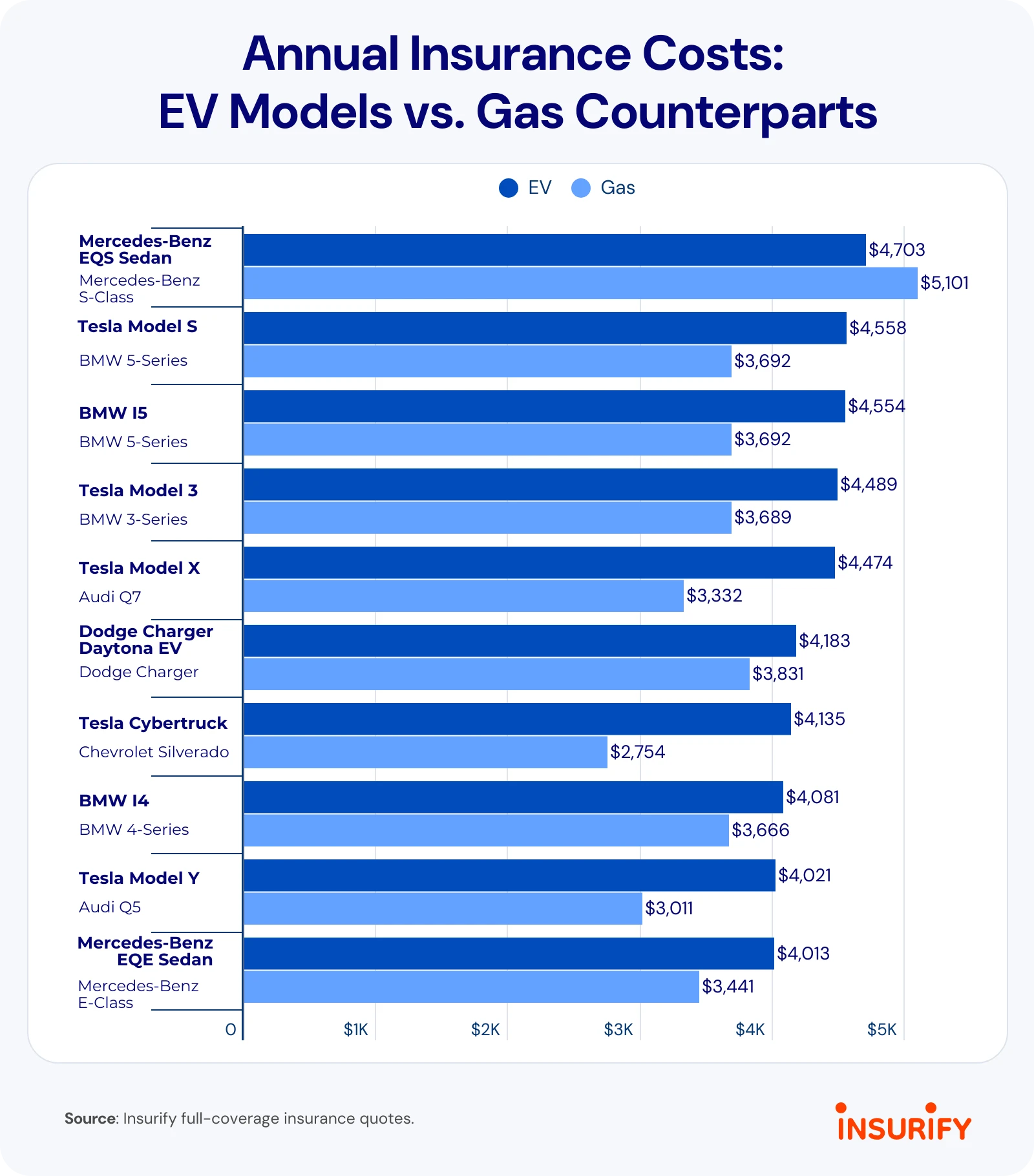

The Most Expensive EVs to Insure

Luxury EVs dominate the list of the most expensive models to cover. The Mercedes-Benz EQS Sedan tops the rankings with an average annual full-coverage premium of $4,703, followed by the Tesla Model S at $4,558 and the BMW i5 at $4,554. According to Insurify, all five Tesla models rank among the 10 priciest EVs to insure.

The comparison with gas-powered vehicles isn’t always straightforward. While most EVs in the ranking cost more to insure than their gas counterparts, the Mercedes-Benz EQS Sedan is actually cheaper to cover than the Mercedes-Benz S-Class, which carries an average annual premium of $5,101.

Elsewhere the EV penalty holds. The Tesla Model S averages $4,558 per year versus $3,692 for a BMW 5-Series, while the Cybertruck costs $4,135 to insure compared with $2,754 for a gas-powered Chevrolet Silverado. The Tesla Model Y also carries a much higher premium at $4,021, against $3,011 for an Audi Q5.

The States Where EVs Are Cheaper

Curiously, there are some states where it’s actually cheaper to run an EV. Montana leads the charge, where EVs come in 4 percent cheaper at $2,242 versus $2,339 for gas cars. The margin is also 4 percent in West Virginia, with premiums of $2,062 for EVs and $2,148 for ICE models. Nebraska slightly favors EVs too, with newer EV premiums of $2,055 against $2,086 for gas-powered cars.

Reading Time: 10minutesClick here to read highlights from the story

Fidelity bonds protect businesses if an employee steals or commits fraud.

The state issues the bonds, and research shows they’re one of the most effective ways to persuade employers to hire people with criminal records.

But Wisconsin issues few fidelity bonds.

Experts are divided on the issue, with some saying the free insurance can’t hurt and might help.

Others say it doesn’t address all the concerns employers have or educate them about the benefits of giving people with criminal records a second chance.

For every 10 people released from Wisconsin’s prisons, just seven find jobs within two years — even as the state’s ongoing worker shortage leaves many employers scrambling to find the help they need.

The struggle isn’t unique to Wisconsin. Formerly incarcerated people nationwide are far more likely to be unemployed than the general population. One reason: Though people with criminal records often outperform their colleagues, many employers worry they’ll be unreliable or even dangerous.

That’s why, 60 years ago, the U.S. government began insuring employers against that risk, for free.

The Federal Bonding Program, established in 1966, offers “fidelity bonds” to reimburse businesses for losses if the covered employee steals or commits fraud.

Recent research suggests these bonds are one of the most effective ways the government can persuade employers to give jobs to people with criminal records. Those jobs have ripple effects. Families become more financially stable, communities become safer — as people with jobs are less likely to commit new crimes — and taxpayers save money as fewer people return to prison.

So why aren’t Wisconsin employers requesting these bonds? While some states issued hundreds last year, Wisconsin issued just three — even though an estimated 1.4 million Wisconsinites have a criminal record.

Demand in the state is so low that when the federal government in 2019 offered Wisconsin $100,000 to spend on bonds, workforce officials used just $15,000.

To figure out what’s going on, Wisconsin Watch spoke to economists, insurance experts, criminologists and workforce development officials, who ranged from enthusiastic to cynical about bonding.

Some said the coverage limits may be too low to address employers’ worries, or that bonds don’t help when employers are worried about safety or a bad work ethic. Some said employers overestimate the risk of hiring people with criminal records and that education — not insurance — is the solution. But most said offering this free insurance can’t hurt and might help.

In a worker-strapped state, is this insurance program a little-known lifeline or an irrelevant relic?

Bonding basics

Imagine you’re a hiring manager who wants to offer a job to an applicant with a criminal record. If you’re in the same boat as many businesses, your commercial insurance may not cover any theft or other act of dishonesty if the employee in question has a criminal record.

To fill that insurance gap, you contact your state’s bonding coordinator to apply for a six-month, no-deductible fidelity bond that will reimburse you for up to $5,000 in losses. In special circumstances, you can apply for additional coverage of up to $25,000. The state handles the paperwork and the $100 cost.

The program boasts a claim rate of just 1%, meaning businesses in the program seldom report losses. At the end of the six months, you may now be satisfied that your new employee is trustworthy — or you can buy additional coverage.

In Wisconsin, these bonds are the only incentive available to encourage what’s often called “second chance” or “fair chance” hiring.

Formerly incarcerated Wisconsinites more likely to be jobless

About 3 out of 10 people released from Wisconsin prisons in 2023 were not employed within two years.

In comparison, only 3 out of 100 people in Wisconsin’s workforce were unemployed.

Source: Wisconsin Department of Corrections

Formerly incarcerated Wisconsinites more likely to be jobless

About 3 out of 10 people released from Wisconsin prisons in 2023 were not employed within two years.

In comparison, only 3 out of 100 people in Wisconsin’s workforce were unemployed.

Source: Wisconsin Department of Corrections

Formerly incarcerated Wisconsinites more likely to be jobless

About 3 out of 10 people released from Wisconsin prisons in 2023 were not employed within two years.

In comparison, only 3 out of 100 people in Wisconsin’s workforce were unemployed.

Source: Wisconsin Department of Corrections

“It is a unique tool to help a job applicant get and keep a job,” the state’s Department of Workforce Development says on its bonding webpage. “It is like a ‘guarantee’ to the employer that the person hired will be an honest worker.”

The same bonds are also available to other job applicants whose background could make it hard to get or keep a job. That includes people in treatment or recovery for alcohol or drug addictions and people with little or no work history.

In practice, the program is almost exclusively used for people with criminal records, according to program administrator Kevin Kulling.

Wisconsin focuses much of its outreach effort on prisons, making sure people know how to take advantage of the program when they get out. The stakes are high: Of those released in 2023, nearly 1 in 3 were rearrested within a year and 1 in 8 ended up back behind bars.

Recent research backs bonds

Governments have tried a variety of ways to persuade employers to hire people with criminal records.

Nationally, there’s the $2-billion-a-year federal Work Opportunity Tax Credit, which rewards employers for hiring people with felony convictions. But new research finds the tax credit doesn’t increase pay or hiring for the workers it’s designed to help. It expired in December but could be reinstated.

Meanwhile, a growing number of states have tried to boost job seekers by barring employers from asking about criminal records on job applications. In about a dozen states, public and private employers are subject to such “ban-the-box” measures.

Evidence is mixed. Several studies find these laws reduce hiring for Black and Hispanic men, suggesting that when employers can’t check an applicant’s criminal record, they instead make assumptions based on demographics.

Enter the bond, a policy that predates the others by decades. In 1975, the U.S. Department of Labor commissioned a study of the then-new program. Participating workers reported major salary increases after joining the program, and a majority held on to their bonded job longer than one year.

New evidence supports the program. In a 2023 article, researchers from the National Bureau of Economic Research teamed up with an online hiring platform to survey businesses. The platform asked users about their willingness to hire people with criminal records and how that might change if the platform offered wage subsidies or insurance coverage.

Researchers found employer willingness to hire someone with a criminal record rose 12% when offered up to $5,000 in crime and safety insurance. It would take an 80% wage subsidy to get the same result.

Mitchell Hoffman, an economics professor at the University of California-Santa Barbara, co-authored that study. He said policymakers have often tried to solve these hiring challenges by trying to change the workers, like with training or therapy. This research suggests it’s possible to change employers’ behavior, too.

That matters, he said, because employers hold the cards. “If firms don’t want to employ people with a record, then it’s hard to move them to employment and to good jobs,” Hoffman said.

The findings are welcome news to Jen Doleac, executive vice president of criminal justice at the philanthropy Arnold Ventures and author of the book “The Science of Second Chances: A Revolution in Criminal Justice.” Doleac, who researches crime and discrimination, was surprised when she first learned about the Federal Bonding Program.

“It’s such a smart idea. Employers say they’re worried about the risk of hiring someone with a record. How do we deal with risk? We provide insurance,” Doleac said. A critic of the Work Opportunity Tax Credit, she said the new research shows why bonds are a better bet.

“Insurance just moved the needle more, and much more dollar for dollar,” Doleac said.

Experts divided

Even in states issuing hundreds of bonds a year, that’s just a fraction of those released from prison annually, and a smaller share of all people with criminal convictions.

“The total number of firms nationally that were involved, it seemed like a very small number,” Hoffman said. “There's interesting variation across states, but overall, just not that much usage.”

Just 27 Wisconsin employers participated in the program in the last five years, according to federal records obtained by Wisconsin Watch. Those businesses range from national retailers like Dollar Tree to smaller agricultural businesses like Rine Ridge Farms.

Why haven’t bonds proven more popular? Wisconsin Watch asked more than a dozen Wisconsin businesses and industry groups about their experience with the Federal Bonding Program. Just one responded, and none agreed to answer questions.

Hoffman thinks maybe employers just aren’t that worried, or that the risk they’re worried about isn’t covered by the bonds. They may worry the applicant will be unreliable or even dangerous, despite evidence to the contrary. In a 2021 survey by the Society for Human Resource Management, more than 80% of business leaders said second-chance hires perform the same as or better than other employees.

“If someone does something bad to a customer,” Hoffman said, that customer might sue, or customers might take their business elsewhere. Bonds don’t cover that risk. “That is very difficult to quantify. What is the cost of that sort of event?”

Another possibility, Doleac said, is that employers don’t know about the bonds. Some states may be doing more to get the word out than others, but marketing costs money that state workforce departments may not have.

The more likely explanation, she said, is that the process is too cumbersome for employers who are used to buying insurance that covers all their employees. Although job applicants and employers do not have to complete any paperwork to get a bond, employers still need to keep track of the policies that were issued to a specific employee.

“It’s just too inconvenient and too much paperwork to keep track of,” Doleac said. She and her colleagues are exploring whether standard policies could include riders covering these workers, without a separate process or schedule.

Meanwhile, some advocates for formerly incarcerated people worry that the bonds can backfire, making employers worry even more.

Craig Coleman, a case manager for Forward Service Corporation, helps formerly incarcerated Wisconsinites get trained and find work. He doubts bonds will help them.

“You’re saying to your employer, ‘If I steal from you, then you'll be reimbursed,’” Coleman said. “I’m not an HR person, but if I had someone come in with an insurance policy saying, ‘If I steal from you,’ that’s the end of the conversation. I'm not hiring you.”

There, she trained more than 50 other companies on “fair-chance hiring,” teaching them that hiring people with criminal records isn’t risky. Talking about extra insurance policies undermines that message, she said.

“Rather than hiring the person because they’re the best person for the job, but they happen to have a record. Now we’re trying to say, ‘Here’s an insurance policy. Please do it,’” Martin said.

The fact that Wisconsin employers seldom use fidelity bonds might even be a good sign. The state has unusually strong organizations that prepare applicants for work and match them with employers, said Josh Morby, who represents such groups as spokesperson for the Wisconsin Workforce Hub. If those organizations are doing their jobs well, employers will trust their participants — no insurance policy necessary.

“Wisconsin employers are looking for candidates who are screened, prepared and supported so hiring justice-impacted talent becomes a reliable workforce solution, not a risk,” Morby said in an email.

Wisconsin bond use lags

The bonding program’s popularity varies among states, according to data Wisconsin Watch obtained from the U.S. Department of Labor’s Employment and Training Administration. In 2025, New Jersey issued 277 bonds, and Washington, D.C., issued 192.

Meanwhile, 12 states didn’t issue any in 2025.

Wisconsin Watch requested interviews with workforce officials in New Jersey, Tennessee, Washington, D.C., and West Virginia to learn why employers there are using more bonds. None responded. A U.S. Department of Labor spokesperson also declined an interview.

One possible explanation for the higher numbers is that those states have higher unemployment rates. But Wisconsin’s unemployment rate was at a historic low in 2018, when the state issued 27 bonds, more than 12 times as many as it did in 2025.

In 2019, Wisconsin workforce officials requested the maximum $100,000 federal grant to buy more bonds. They said they planned to buy 1,000 bonds over four years, plus more with other funds. They estimated more than 5,500 Wisconsinites with criminal records were eligible. The bonds, they said, would help break “the cycle of recidivism.”

But the COVID-19 pandemic — which shuttered businesses and locked down prisons — derailed the state’s plans.

“With the unemployment rate at an increased rate in Wisconsin, many recruitment efforts for employers to use Fidelity Bonds (have) slowed,” officials wrote in each quarterly grant report from April 2020 to February 2021.

When the grant period ended in 2023, Wisconsin had issued just 59 bonds. Officials wrote that, despite their outreach efforts, their bond numbers were “extremely low.”

The bond’s popularity has since further waned. In each of the last two years, Wisconsin issued no more than three bonds. Department spokesperson Haley McCoy attributed that to the state’s tight labor market.

“Given the strong demand to fill vacant positions, employers have not needed the added incentive of fidelity bonds to hire justice-involved employees during this historically strong economic period,” McCoy wrote in an email to Wisconsin Watch.

Asked whether the Department of Workforce Development plans to make any changes to Wisconsin’s bonding program, McCoy said the bonds are “just one tool in the toolbox that can help a job seeker secure a job.”

“We’ll continue to work with our partners to provide opportunities and prepare job seekers and workers for their next opportunity in Wisconsin,” McCoy wrote.

From a job market ‘hidden force’ to a lever against bias

Meanwhile, Arnold Ventures researchers are trying to figure out how to get more businesses across the country to use federal fidelity bonds or something similar.

Criminal justice director Carson Whitelemons has been studying ways to improve the federal program. But she said just trying to understand how bonding works and how it fits with existing business policies can be “incredibly difficult.”

“Even for business owners who are trying to ask their insurers what is covered and what is not covered, it's not always clear, and often that realm of uncertainty, I think, is what makes employers cautious,” Whitelemons said.

But it’s not just about bonding. The work is part of a new effort she’s organizing with experts from a variety of fields, trying to understand the biases that can keep people from getting all kinds of coverage and how to fix them.

“(Insurance) is such a powerful lever in terms of what people feel safe or empowered to do, what they feel protected from. This has come up again and again in terms of different issues in the United States, in home ownership and redlining — insurance is often this hidden force, especially in areas where there is stigma or discrimination.”

Hoffman, the HR economist, said if more employers use bonds, that could help dispel misconceptions about people with records.

“Employers … think they’re less productive than they actually are,” Hoffman said. That’s not the problem bonds are designed to solve, but if bonding gets more employers to hire these applicants, the experience may change how they view similar applicants in the future, he said.

Meanwhile, officials from Wisconsin’s Department of Corrections will continue teaching prisoners about these seldom-used bonds and encouraging them to pitch the opportunity to their potential future bosses — for better or worse.

Hongyu Liu is a data investigative reporter for Wisconsin Watch. Email him at hliu@wisconsinwatch.org.

Natalie Yahr reports on pathways to success statewide for Wisconsin Watch, working in partnership with Open Campus. Email her at nyahr@wisconsinwatch.org.

Wisconsin Watch is a nonprofit, nonpartisan newsroom. Subscribe to our newsletters for original stories and our Friday news roundup.